How is the Iran War affecting gas prices and real estate, and what does history suggest about the Iran war impact on home prices?

The clearest short-term link is this: war-driven oil shocks raise gas prices, which can feed inflation, pressure mortgage rates, and cool buyer demand. So far in 2026, U.S. home sales have softened, inventory has improved only modestly, and builders report more pricing pressure—even though home prices nationally have not collapsed.

The Iran War Is Primarily Hitting Real Estate Through Energy Costs

The current conflict’s biggest housing effect is not that buyers suddenly stop needing homes. It is that higher energy costs ripple through the economy fast.

As of April 21, 2026, AAA’s national average for regular gas was $4.022 per gallon. That is down from the mid-April spike, but still well above late-February levels. AAA reported the national average climbed from $2.98 on February 26 to $3.98 on March 26, then above $4.08 on April 2, the first time it topped $4 since August 2022.

On the oil side, EIA said its April outlook expected Brent crude to rise from an average of $81 per barrel in 1Q26 to a peak of $115 in 2Q26, assuming the conflict faded after April and transit through the Strait of Hormuz gradually resumed. EIA’s 2026 average forecast rose to $96 Brent and $3.70 retail gasoline, versus $69 Brent and $3.10 gasoline in 2025.

That matters for real estate because higher oil and gas prices affect housing in three ways:

- they squeeze household budgets,

- they increase inflation pressure,

- and they raise costs tied to construction, transport, and materials.

Oil and Real Estate: Mortgage Rates Are the Pressure

Point

The fastest transmission channel from oil and real estate is mortgage rates.

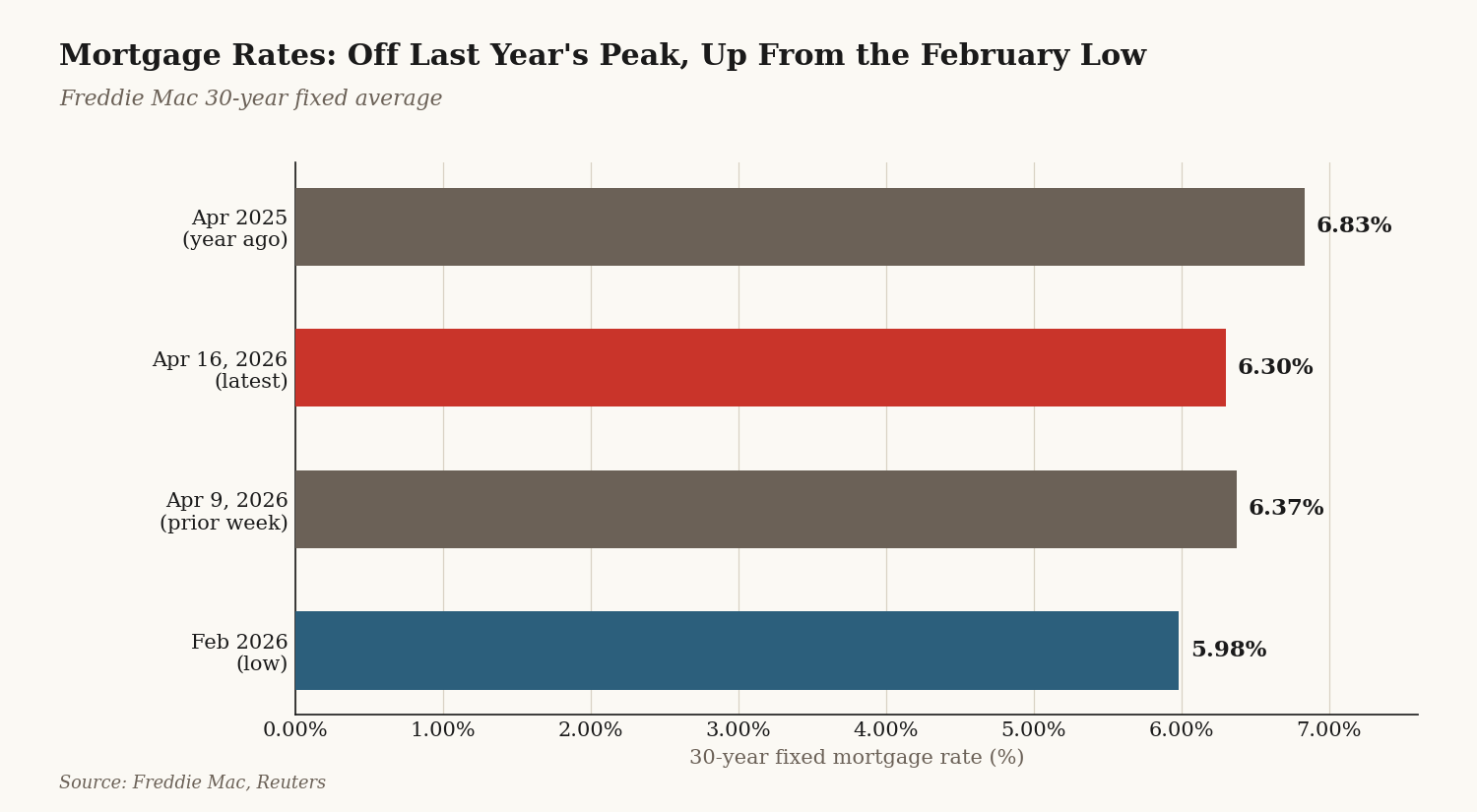

Freddie Mac said the average 30-year fixed mortgage rate was 6.30% on April 16, 2026, down slightly from 6.37% a week earlier but still well

above the 5.98% level Reuters cited from February. A year earlier, the 30-year rate was 6.83%.

That may sound manageable compared with 2023 or 2024, but the problem is affordability. NAR’s Housing Affordability Index fell to 113.7 in March from 117.5 in February, showing that even with rates below last year’s levels, affordability worsened month to month as financing costs and prices stayed elevated.

This is why the housing market can feel weak even when prices do not fall sharply:

- higher rates reduce buying power,

- higher gas prices squeeze monthly budgets,

- and uncertainty makes buyers more cautious.

Builders Are Feeling the Energy Shock Too

The resale market is only part of the picture. New construction is also reacting to the oil spike.

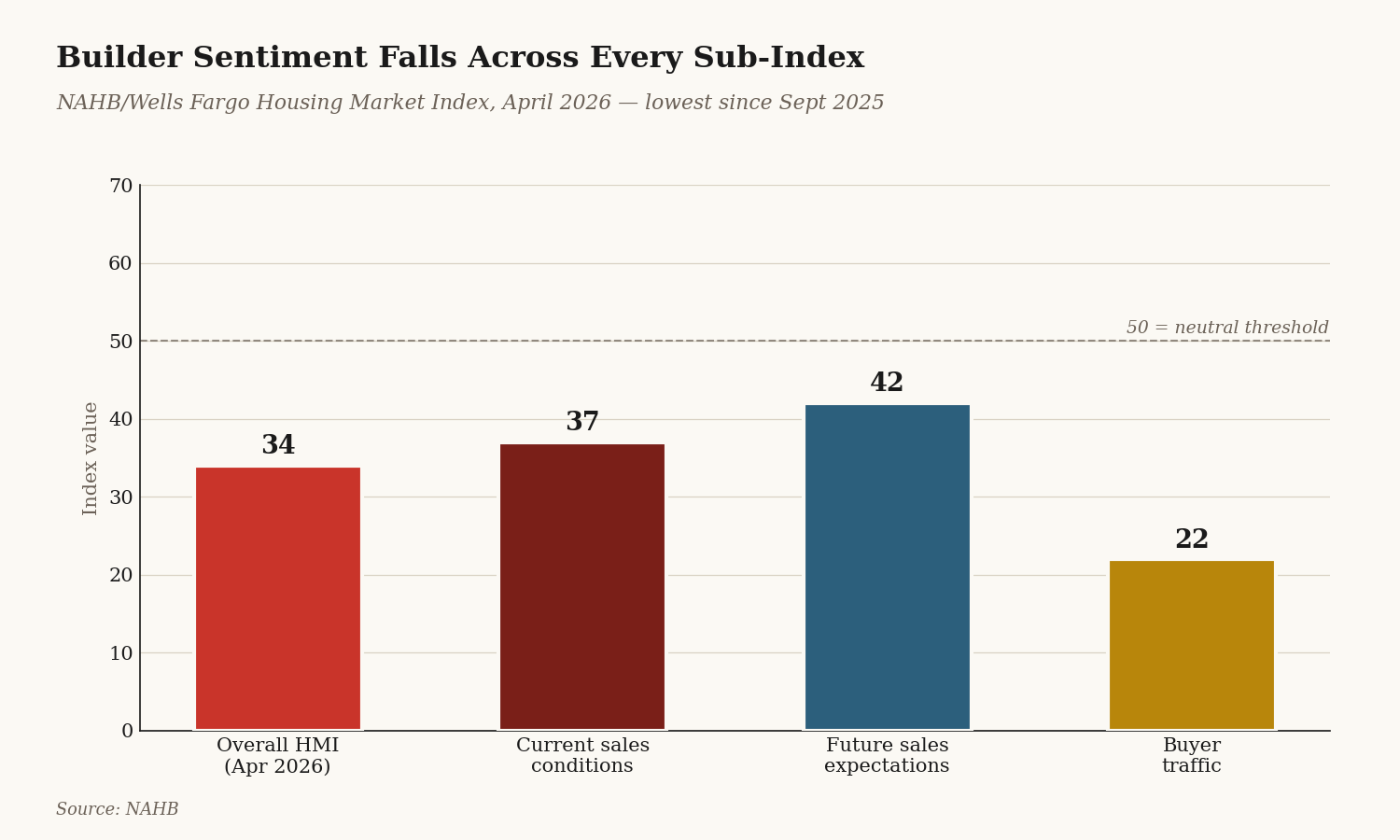

NAHB said builder confidence for single-family homes fell to 34 in April, down four points and the lowest since September 2025. The subindex for current sales conditions fell to 37, future sales expectations dropped to 42, and buyer traffic slipped to 22.

The cost side is where the Iran conflict becomes especially relevant to housing supply. NAHB reported:

- 62% of builders said suppliers had increased material costs because of higher fuel prices,

- 70% of builders said uncertainty around costs made home pricing more difficult, and energy costs account for about 4% of residential construction material input and service costs.

That matters because if builders face rising delivery, diesel, and materials costs, they are less likely to aggressively cut prices. So even when demand slows, supply may not expand enough to create major nationwide price declines.

What Happened During Earlier Middle East Wars?

History does not repeat perfectly, but it does give useful patterns.

Gulf War: 1990–1991

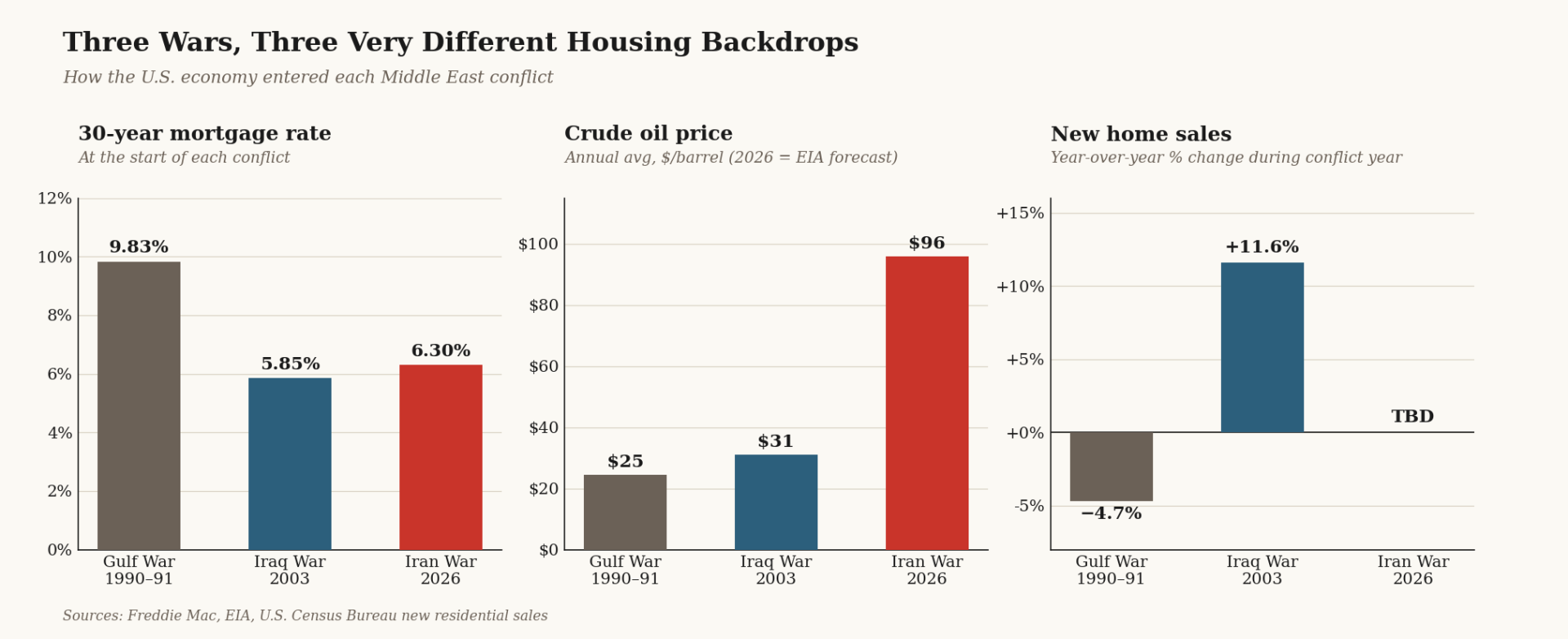

During the Gulf War period, annual WTI crude rose from $19.64 in 1989 to $24.53 in 1990, then eased to $21.54 in 1991. Mortgage rates were also high by modern standards: Freddie Mac’s 30-year mortgage series shows 9.83% on January 5, 1990 and 9.56% on January 4, 1991, falling to 8.35% by December 27, 1991.

Housing activity slowed, especially in new construction. New single-family home sales fell from 534,000 in 1990 to 509,000 in 1991, a decline of about 4.7%. National home prices, however, did not crash: the U.S. all-transactions house price index moved from 165.05 in Q1 1990 to 171.28 in Q4 1991. California was much weaker, rising only from 227.32 to 228.66 over that span before falling in later years.

The takeaway: an oil shock and high rates slowed sales more clearly than they crushed national prices.

Iraq War: 2003

The 2003 Iraq War looked very different because mortgage rates were much lower and the broader housing cycle was already strong.

Annual WTI crude rose from $26.18 in 2002 to $31.08 in 2003. Yet Freddie Mac’s 30-year rate started 2003 at 5.85% and ended the year near 5.81%. New home sales actually rose from 973,000 in 2002 to 1.086 million in 2003. The U.S. house price index rose from 279.39 in Q1 2003 to 295.28 in Q4 2003, while California surged from 366.88 to 411.10.

The lesson there is critical: Middle East conflict alone does not determine what home prices do. The bigger factor is the starting point for rates, supply, and domestic housing demand.

So What Does the Iran War Impact on Home Prices Likely Look Like Now?

Based on the current numbers, the most defensible conclusion is this:

- Sales volume is weakening. Existing-home sales fell to 3.98 million in March, and pending sales were down 4.1% in early April.

- Inventory is improving, but not enough to reset the market. Existing inventory is at 1.36 million homes and 4.1 months of supply, which is better than earlier conditions but still not a glut.

- Prices are decelerating, not broadly collapsing. NAR’s median existing-home price was up 1.4% year over year, and Redfin’s national median sale price was up 1.2% in March.

- Builders face cost pressure that can keep supply tight. Higher fuel costs are feeding into construction and pricing decisions.

So the likely near-term effect of the Iran War is slower transactions, more cautious buyers, and modest pressure on price growth—not necessarily a dramatic nationwide drop in home values.

The Bigger Picture: Is Real Estate Still a Safe Investment?

Even with all this uncertainty, real estate continues to behave differently than other assets.

Here’s what you should keep in mind:

- Real Estate Is a Long-Term Asset

- Short-term volatility—like what we’re seeing with the Iran War—can impact activity, but housing markets typically stabilize over time.

- Inflation Can Support Home Values

As costs rise across the economy:

- Replacement costs increase

- Construction becomes more expensive

- Existing homes often retain value

Demand Doesn’t Disappear

People still need housing regardless of global events.

Final Takeaway

The strongest evidence today suggests that the Iran War, gas prices and real estate are linked most directly through affordability and activity, not through an immediate collapse in home prices.

That pattern also fits history. In the 1990–1991 Gulf War, housing activity weakened more than national home prices. In 2003, housing powered ahead because rates were low and demand was strong. In 2026, the market starts from a tougher place: affordability is already stretched, rates are still elevated, and inventory remains below normal. That makes the housing market more vulnerable to oil shocks—but still not automatically headed for a crash.

Sources

- National Association of Realtors (NAR) – Existing Home Sales Reports

-

Federal Reserve Economic Data (FRED) – Mortgage rates, home price index

-

U.S. Energy Information Administration (EIA) – Oil forecasts

-

AAA – National gas price data

-

Redfin Housing Market Reports

-

National Association of Home Builders (NAHB) – Builder sentiment index

-

Freddie Mac – Mortgage Market Survey

Hot Air and Cold Truths: What Your HVAC Isn’t Telling You