Will the Fed cut interest rates in 2026?

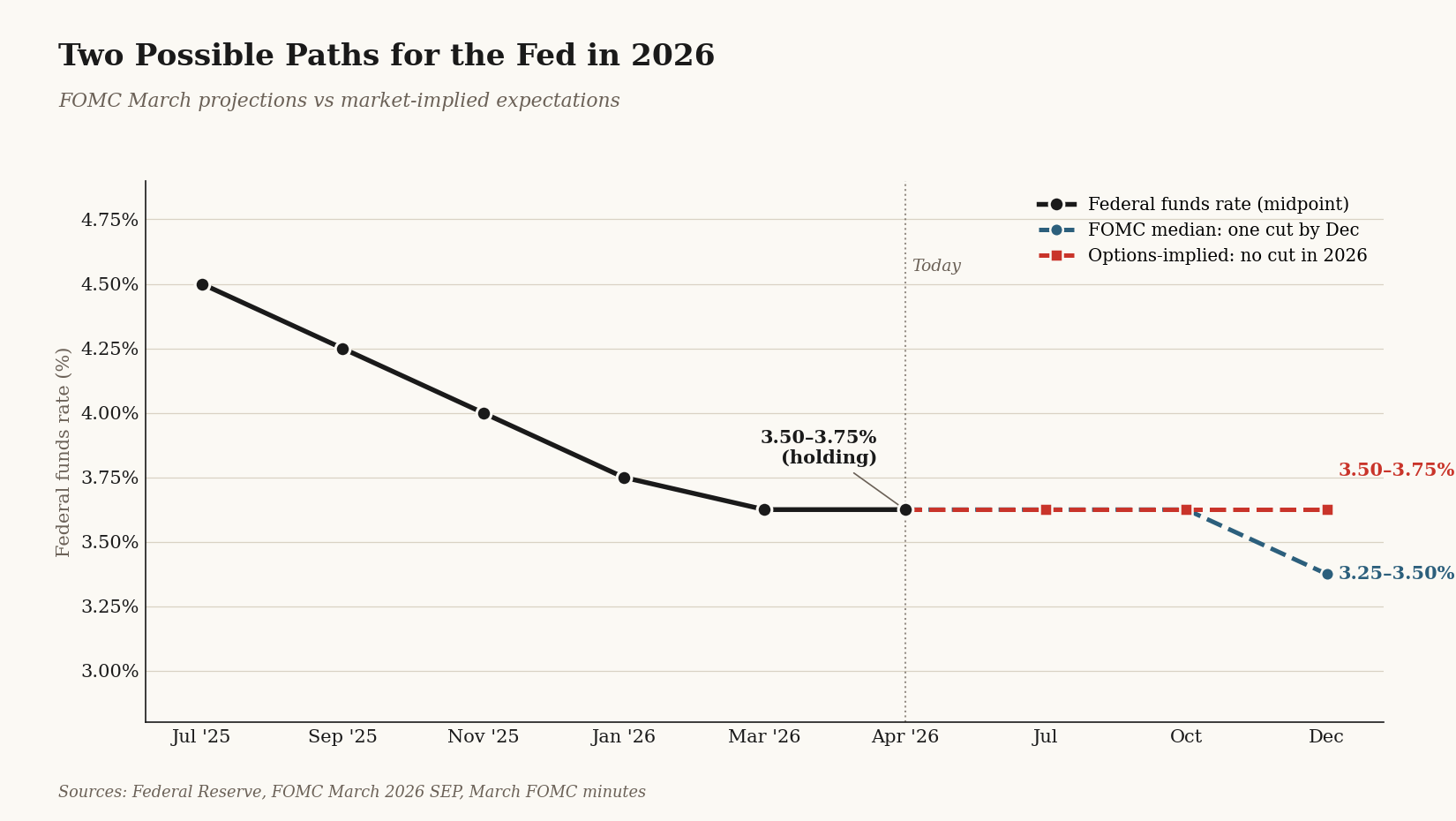

The most honest answer right now is maybe, but it is no longer the base-case certainty many people assumed earlier in the year. As of April 21, 2026, the Federal Reserve is still holding its benchmark rate at 3.50% to 3.75%, its March projections still pointed to a median expectation of one cut this year, but markets and several economists have recently shifted toward expecting no cuts at all because inflation risks remain sticky.

Why the Fed may not cut this year

The Fed’s challenge is simple: it wants inflation back to 2%, but recent data and policymaker comments suggest price pressure is still running too hot to declare victory. In mid-April, St. Louis Fed President Alberto Musalem said core inflation could stay near 3% for much of 2026, and the March FOMC minutes noted that futures markets had shifted enough that a cut was not fully priced in until December, while options markets were consistent with no rate change this year.

That is why the better question for your clients is not “Will rates definitely fall?” but “What happens if they do not?” The Fed itself is still signaling a cautious, data-driven stance, saying it will carefully assess incoming data, the evolving outlook, and risks before making additional adjustments.

What that means for mortgage rates

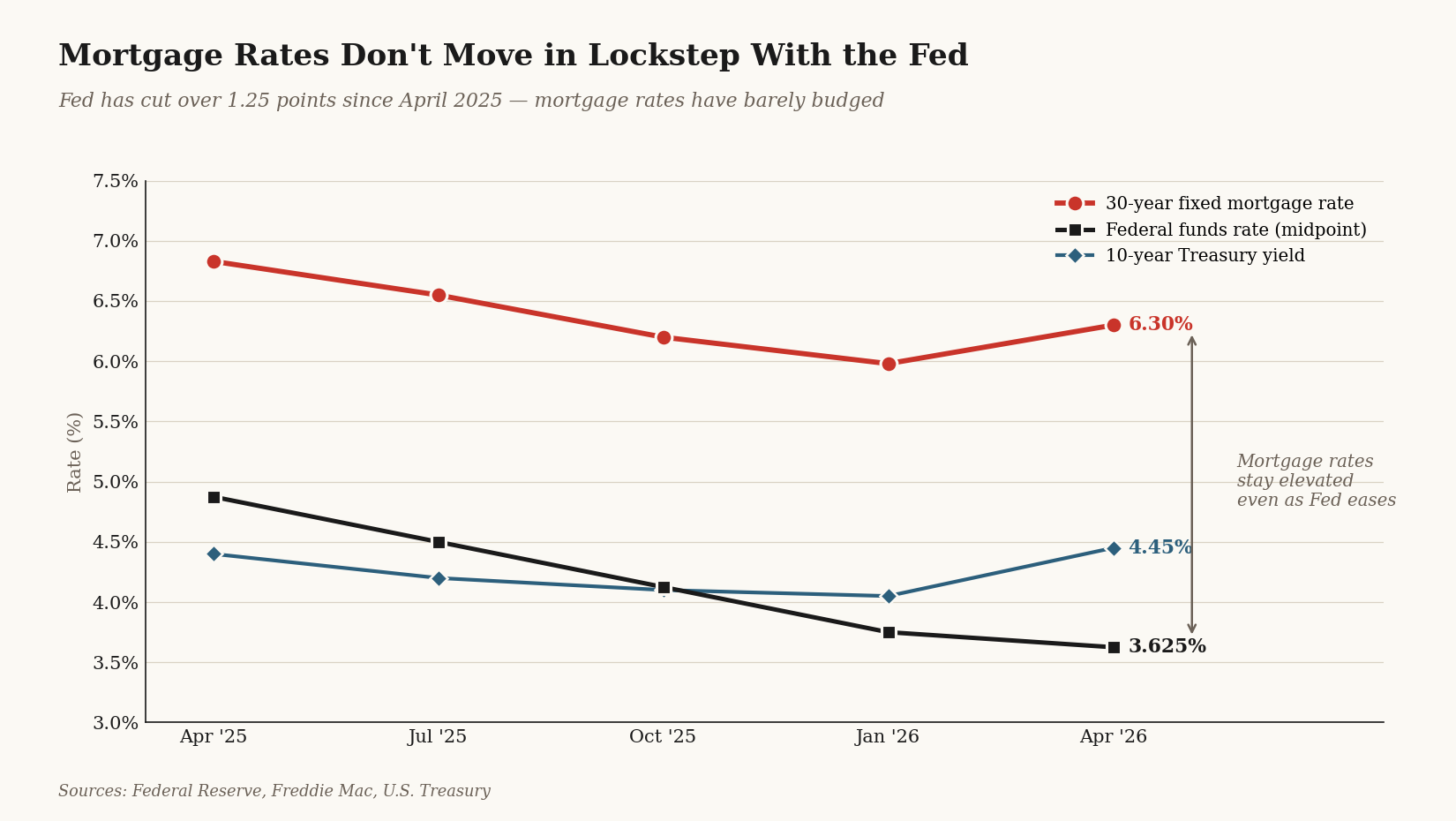

One of the biggest misconceptions in real estate is that the Fed directly sets mortgage rates. It does not. The Fed controls a short-term benchmark, while 30-year mortgage rates are influenced more directly by longer-term bond yields, especially the 10-year Treasury, along with inflation expectations and broader market risk. That is one reason mortgage rates can stay elevated even when the Fed pauses or even cuts.

Right now, the average 30-year fixed mortgage rate is about 6.30%, according to Freddie Mac’s April 16, 2026 survey. That is down from a year ago, but still high enough to keep affordability tight for many buyers.

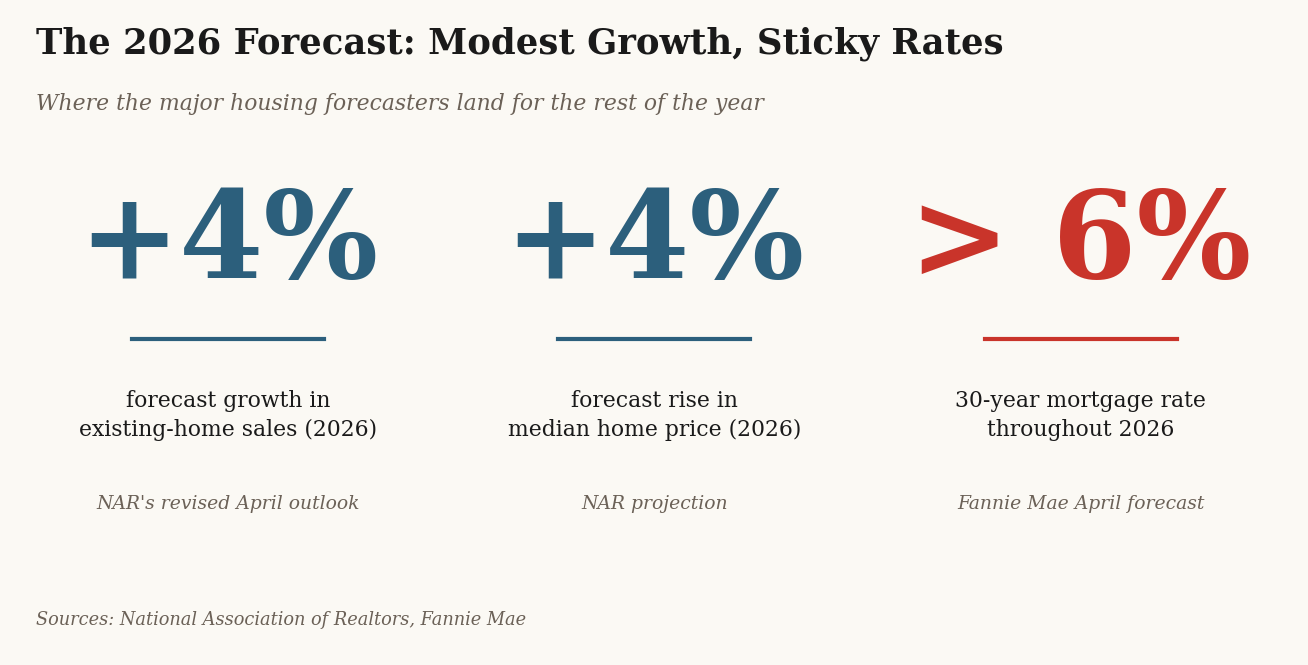

So even if the Fed does manage one cut later this year, that does not guarantee a dramatic drop in mortgage rates. And if the Fed makes no cuts, mortgage rates could remain in the mid-6% range or move around based more on inflation data, Treasury yields, and investor sentiment than on Fed headlines alone. Fannie Mae’s April 2026 housing forecast said rates are now expected to stay above 6% throughout 2026, even though some easing later in the year is still possible.

How a no-cut year would affect the housing market

If the Fed does not cut, the housing market likely stays in its current pattern: slower sales, persistent affordability pressure, and continued importance of motivated buyers and sellers rather than broad-based momentum. Existing-home sales fell 3.6% in March 2026, and NAR said lower consumer confidence and softer job growth were already holding buyers back. At the same time, the median existing-home price still rose 1.4% year over year to $408,800, which shows that weak affordability has not automatically translated into falling prices.

That combination matters. When borrowing costs stay high, many would-be sellers stay put because they do not want to give up their older, lower mortgage rate. That limits inventory. And when inventory stays constrained, prices can remain surprisingly firm even in a slower market. NAR recently revised its 2026 forecast to a more modest 4% increase in existing-home sales this year, largely because mortgage rates have stayed higher than originally expected, while still projecting home prices to rise 4% in 2026.

In plain English: no Fed cut does not necessarily mean a housing crash. It more likely means a market where affordability stays tough, move-up buyers stay selective, first-time buyers feel the most pressure, and pricing becomes more hyper-local and strategy-driven.

What buyers and sellers should take away

For buyers, waiting for a dramatic rate drop could be a risky strategy. If rates stay near current levels and inventory remains limited, you may still face competition on well-priced homes. For sellers, a no-cut environment means pricing, preparation, and presentation matter even more because buyers are more payment-sensitive than ever. Recent data still shows demand is present, but it is cautious demand. Pending home sales rose 1.5% in March, even as mortgage costs remained elevated, which suggests serious buyers are still active when the right opportunity appears.

Final takeaway

The best read today is this: the Fed could cut later in 2026, but that outlook is much less certain than it looked earlier, and a no-cut year is absolutely on the table. If that happens, the housing market will likely remain challenged by affordability and uneven activity rather than shift into a sudden boom or bust. In other words, this is still a market that rewards strategy over speculation.