The LA Insurance Question Every Buyer and Seller Now Has to Answer

If you've tried to buy or sell a home in Los Angeles in the last six months,

you've probably hit a moment that didn't exist a few years ago: the deal is

going smoothly, the inspection is fine, the appraisal lines up — and then the

buyer's lender comes back with a problem. The buyer can't get homeowners

insurance. Or they can, but only through the FAIR Plan, and only at a price

that changes the deal entirely.

This isn't a niche issue anymore. It's the question reshaping LA real estate

transactions in 2026, and most buyers and sellers are walking into it

unprepared.

What's actually happening

After the Palisades and Eaton fires in early 2025 — which together caused about

$40 billion in insured losses and destroyed roughly 12,000 homes — California's

homeowners insurance market entered a kind of slow-motion contraction. Major

carriers cut back where they would write new policies. Some left the state

entirely. Renewals started getting denied for properties that, on paper,

weren't in obvious wildfire zones.

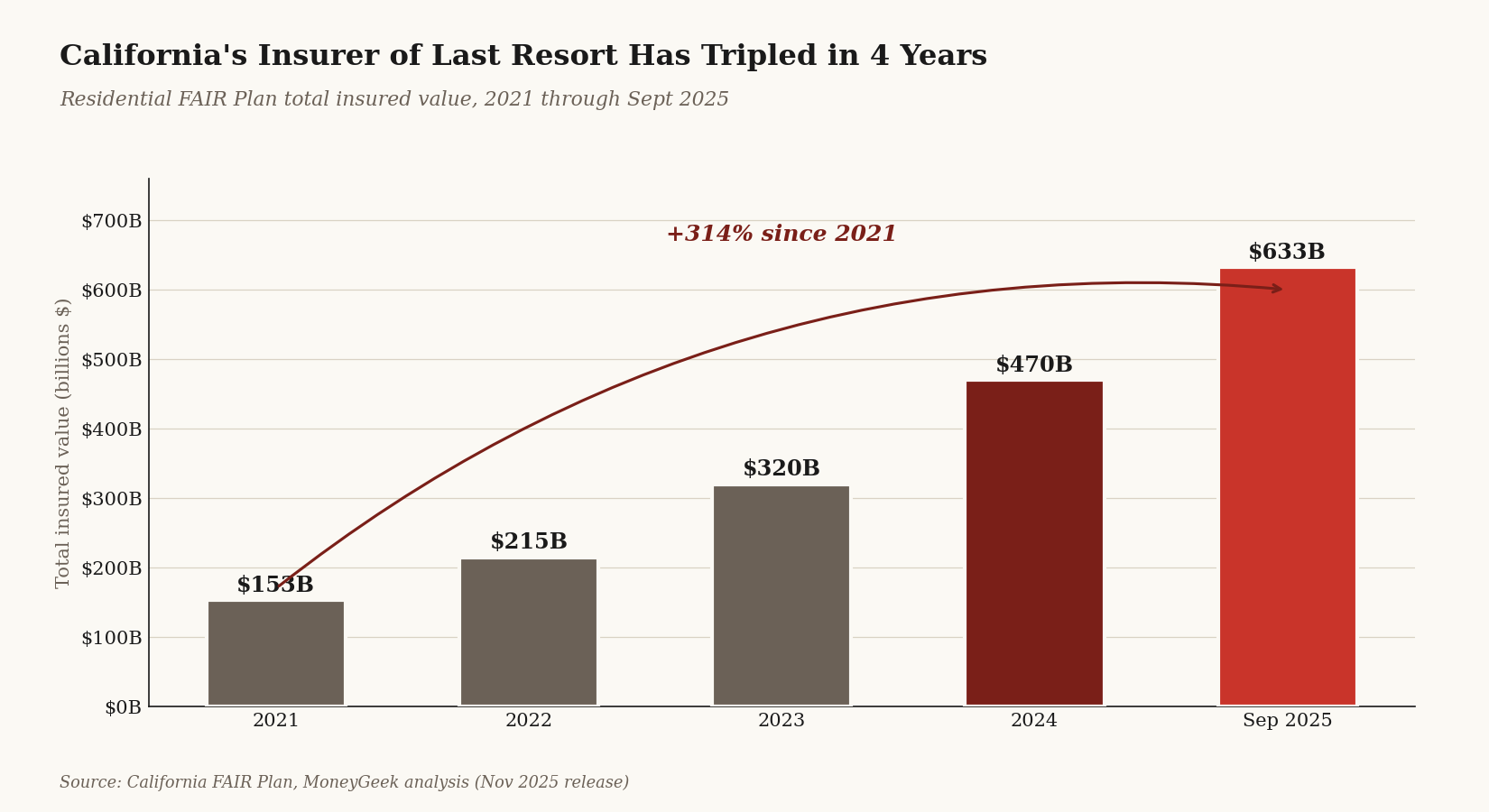

The result has been a surge into the California FAIR Plan, the state-backed

insurer of last resort. FAIR Plan enrollment grew 43% between September 2024

and December 2025. In just the final three months of 2025, the plan added

nearly 22,000 new residential policies. Total residential exposure on the FAIR

Plan reached $633 billion as of September 2025 — up 314% since 2021.

The most striking part isn't the growth. It's where it's coming from. Roughly

14% of current FAIR Plan policies now cover properties in largely urban,

lower-fire-risk neighborhoods — areas that used to be considered

"normal" parts of the insurance market. Those policies make up about

28% of the plan's total exposure. In other words, the pullback isn't confined

to canyon homes and hillside properties. It's spilling into flat parts of LA

that homeowners always assumed were safe bets for coverage.

Why this matters at the closing table

For buyers, the practical consequence is this: you can no longer assume you'll be able to get insurance on a property at a reasonable cost, and your lender won't fund the loan without it. That means the coverage question has to move from "we'll handle that during escrow" to "let's confirm this before we make an offer."

For sellers, the consequence is the mirror image. If a buyer can't get coverage on your property, the deal stalls. If they can only get coverage through the FAIR Plan plus a wraparound policy for theft and liability, the total annual cost can be high enough to change what they're willing to pay. Sellers who haven't thought through their property's insurance profile in advance are losing leverage in negotiations and, in some cases, losing deals entirely.

This is true even for properties nowhere near brush. A home in Mar Vista or Mid-City can run into the same problem as one in Topanga, just for different reasons — older roof, prior claims history, ZIP-code-level non-renewal patterns by a particular carrier.

The new state laws that change the conversation

On January 1, 2026, nine new insurance laws took effect in California. Most homeowners haven't heard of them, but several directly affect transactions happening right now:

The **California Safe Homes Act (AB 888)** created a state grant program to help eligible homeowners pay for fire-safe roof replacements and "Zone Zero" mitigation — the first five feet around the home. Applications are expected to open in spring 2026. The grants are aimed at low- and moderate-income homeowners in high or very-high fire hazard ZIP codes.

The **Insurance and Wildfire Safety Act (AB 1)** requires the state to regularly update its Safer from Wildfires regulations, which determine what mitigation work qualifies for insurance discounts.

The **Eliminate "The List" Act (SB 495)** requires insurers to pay 60% of contents coverage limits — capped at $350,000 — to total-loss wildfire survivors without requiring a detailed inventory list. Anyone who watched friends fight to itemize a destroyed home after the 2025 fires understands why this matters.

There are also new rules taking effect July 1, 2026 that require residential replacement-cost policies to include building-code-upgrade coverage of at least 10% of the dwelling limit — meaning if you have to rebuild, your insurance has to help pay for the modern code requirements that didn't exist when your house was built.

A separate bill, **SB 876**, is moving through Sacramento now and would speed up claim payouts further, expand Additional Living Expenses coverage by 100% in declared disasters, and require insurers to make upfront payments on actual cash value and structure replacement cost following a total loss.

What buyers should be doing differently

Three things, in order of importance.

- First, get an insurance quote before you write an offer, not during escrow. A licensed broker can run the property's address through their carriers in 24–48 hours and tell you what's available, at what price, and with what conditions. If the only available option is the FAIR Plan plus a wraparound, you want to know that before you commit, not after.

- Second, ask the seller for the property's CLUE report — the loss history database insurers use. A few minor claims in the last seven years can be the difference between a normal policy and a non-standard one. Sellers can pull their own report for free; buyers normally can't.

- Third, factor the insurance cost into your monthly payment math. A FAIR Plan policy plus the wraparound can run two to four times what a standard policy would have cost five years ago. That changes affordability calculations in a way that mortgage calculators don't capture.

What sellers should be doing differently

If you're getting ready to list, treat insurance as part of your pre-listing prep, not an escrow problem.

Start by pulling your own CLUE report through LexisNexis (you're entitled to one free copy per year). If there are old claims showing, you'll want to know what a buyer's broker is going to see. If something on the report is wrong — and errors are common — you have time to dispute it before it kills a deal.

Next, document the mitigation work you've already done. New roof? Save the permit and material specs. Cleared brush within five feet? Take dated photos. Replaced wood vents with ember-resistant ones? Keep the receipts. This documentation does two things: it strengthens your buyer's ability to qualify for a standard policy, and if you've done the work that aligns with the state's Safer from Wildfires regulations, it can directly support insurance discounts.

If your property is in a high or very-high fire hazard ZIP code and you haven't done Zone Zero work, the new Safe Homes grant program may help fund it. The application portal hadn't opened as of early 2026, but it's worth tracking — the work both improves your home's insurability and makes it more attractive to buyers who are now scrutinizing this.

Finally, if your current carrier has a non-renewal pattern in your ZIP code, your buyer is going to find out. It's better to surface that yourself, in your disclosures, than have it come up as a surprise in escrow.

The bigger picture

California's insurance commissioner has been pushing reforms — the Sustainable Insurance Strategy, allowing catastrophe modeling in rate-setting, requiring insurers seeking rate increases to commit to writing more policies in distressed areas. Some carriers have responded. Others haven't. The pace of FAIR Plan growth slowed in late 2025, but it hasn't reversed.

For LA real estate specifically, this means the market has quietly developed a new variable that didn't exist three years ago. Price, location, condition, and now insurability — and the fourth one can override the first three.

The buyers and sellers who are navigating this well aren't waiting for the market to settle. They're building insurance into the transaction from day one, asking the right questions before they sign anything, and treating the new state programs as tools they can actually use rather than headlines they read once and forgot. The ones who treat insurance as a footnote are the ones losing deals.

If you have a transaction coming up — whether you're buying,

selling, or just thinking about timing — the insurance question is now part of

it. Plan accordingly.

*This post is for general information only and isn't insurance, legal, or financial advice. Insurance availability and pricing depend on the specific property, carrier, and your individual situation. Talk to a licensed insurance broker about your home.*

Before You Fall in Love with a House, Do This First.