The basic idea: defensible space, in zones

When wildfire researchers and fire departments talk about protecting a home from fire, they think in concentric rings around the structure. Each ring has a different job and different rules.

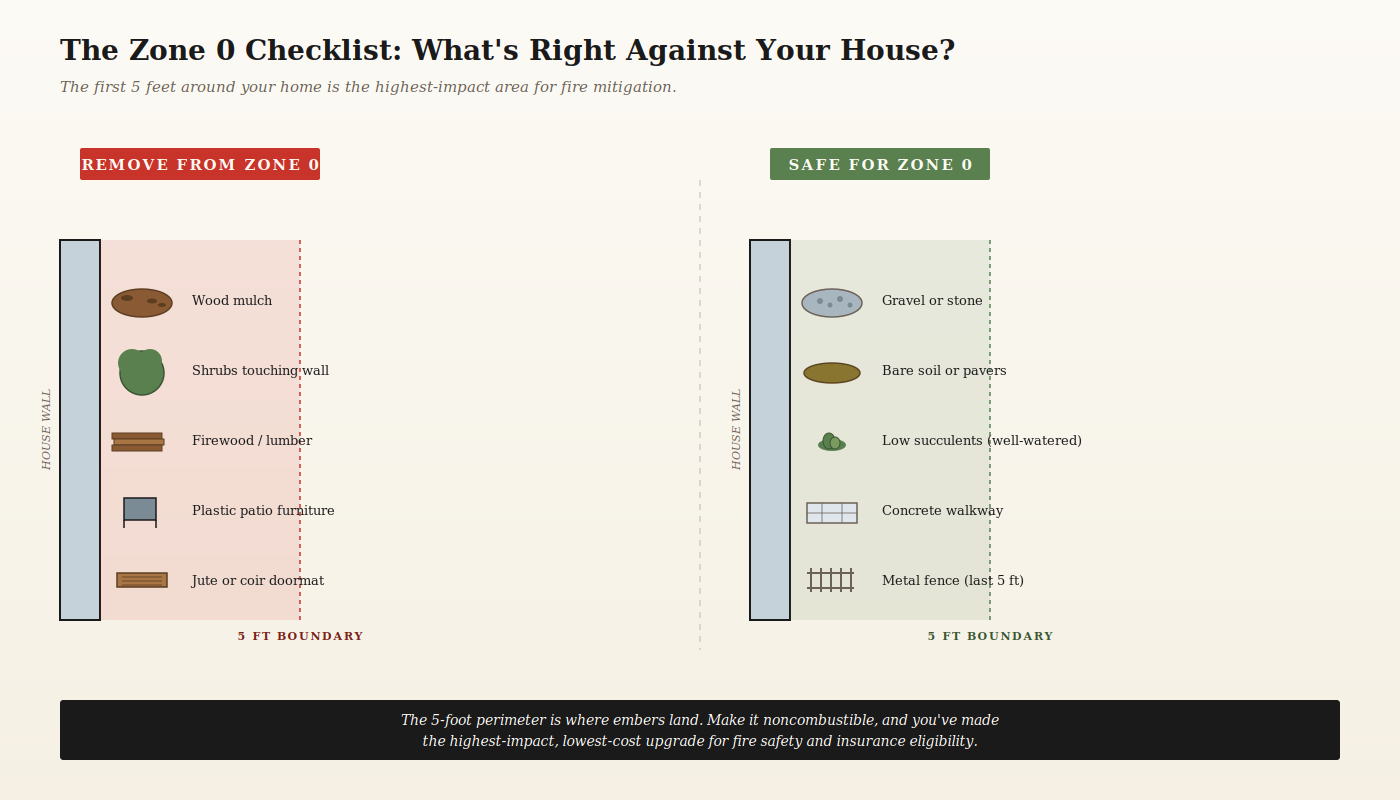

Zone 0 is the first 5 feet around your home — the area right against the foundation, walls, and decks. This is the most critical zone, because it's where embers (which can travel a mile or more on the wind) tend to land and ignite things touching the house. The goal in Zone 0 is to have nothing that can catch fire: no wood mulch, no shrubs against the wall, no firewood piles, no plastic patio furniture, no jute doormats. Concrete, gravel, stone, bare soil, and small succulents are fine.

Zone 1 runs from 5 to 30 feet out. This is the "lean, clean, and green" zone. Plants are okay, but they need to be well-spaced, well-watered, and trimmed. Tree branches should be pruned to at least 10 feet above the ground. Dead leaves and debris cleared.

Zone 2 runs from 30 to 100 feet out (or to your property line, whichever is closer). This is more about thinning and reducing the "fuel ladder" — the path fire takes from the ground up into trees and onto your roof.

For a typical LA homeowner, Zone 0 is where the conversation starts. It's the zone with the highest impact, the lowest cost, and the strongest connection to insurance eligibility.

Why this matters in 2026

Two things changed at the start of 2026 that make home hardening more financially relevant than it's ever been.

First, California's homeowners insurance market has tightened dramatically since the January 2025 fires. Insurers are increasingly using mitigation status — what work has been done, documented, and verified — as a factor in whether they'll write a policy at all, not just what they'll charge. The state's Safer from Wildfires regulations, updated through new laws like AB 1, require insurers to offer discounts for specific mitigation work. But discounts are only useful if you've done the work and can document it.

Second, the California Safe Homes Act (AB 888) took effect January 1, 2026. It created a state grant program — administered by the Department of Insurance — to help eligible homeowners pay for two specific things: fire-safe roof replacement, and Zone 0 mitigation work. The application portal is expected to open in spring 2026.

The grants are prioritized in this order: roof replacement first, then the 5-foot noncombustible zone. Eligible applicants are property owners in ZIP codes that overlap with high or very-high fire hazard severity zones, with the property covered by either an admitted insurer or the FAIR Plan. The program is aimed at low- and moderate-income homeowners, but the income thresholds and exact grant amounts hadn't been finalized as of early 2026.

In other words, the state is now actively paying homeowners to do the same work insurers are increasingly demanding. That alignment is new, and it's worth taking advantage of.

What the work actually looks like

Here's a practical Zone 0 checklist for a typical LA single-family home. Most of these items are not expensive on their own; the cost adds up because there are several of them.

Replace combustible material right against the house. That means swapping wood mulch for gravel or stone, removing shrubs and bushes that touch the siding, pulling firewood and lumber piles away from the structure, and getting rid of doormats, planters, and patio furniture made of plastic, jute, or untreated wood within 5 feet of any wall.

Clear under and around decks. Decks are one of the highest-risk features of a home in a fire. Anything stored underneath — bikes, paint cans, old furniture, dried leaves — needs to come out. The space under the deck needs to stay clean year-round.

Address the roof and gutters. Most roof fires don't start because flames hit the roof. They start because embers land in dry leaves and pine needles in the gutters, then ignite the roof edge from above. Annual gutter cleaning matters more than people realize. If your roof itself is wood shake or composite that's near end-of-life, replacement with a Class A fire-rated roof (asphalt shingle, metal, tile, or concrete) is the single biggest hardening upgrade you can make — and it's exactly what the Safe Homes grant program is designed to help fund.

Upgrade vents. Standard attic, foundation, and soffit vents are designed to let air in and out, which means they also let embers in. Ember-resistant vents (look for the WUI 1/8-inch mesh standard) prevent that. Replacement cost runs roughly $30–$80 per vent, plus labor.

Re-evaluate fencing. Wood fences that connect directly to the house are essentially a fuse leading to your siding. The fix isn't always to replace the whole fence — often it's to replace just the last 5 feet of fence nearest the structure with metal or masonry, breaking the path.

A realistic budget

The "$5,000 project" framing isn't a precise number — your costs will vary based on your home's size, age, and current state. But for most LA single-family homes that haven't done any hardening work, the total comes out roughly like this:

A full Zone 0 mulch and landscape redo with gravel or stone substitution: $1,500 to $3,500 depending on square footage and whether you do the labor yourself. Replacing 8 to 12 standard vents with ember-resistant versions: $500 to $1,500 installed. Replacing the last 5 feet of wood fencing with metal panels: $400 to $1,200. Annual gutter guards: $300 to $1,000. Trimming back tree branches and clearing debris within Zone 1: $500 to $1,500.

That's roughly $3,200 to $8,700, depending on how much DIY work you do and how much you outsource.

Roof replacement is a separate, much larger expense — typically $15,000 to $40,000 for an LA-area home — but it's also the single biggest insurability factor for many properties, and it's the top priority for the Safe Homes grant program.

How to actually take advantage of the grants

A few practical steps you can take now, even before the application portal opens.

Document your starting condition. Take dated photos of your roof, eaves, soffits, vents, and the 5-foot perimeter around your home. If you do the work yourself before the grant opens, you'll need before-and-after evidence. (Note that most state grant programs require approval before work begins to qualify for reimbursement, so check the program rules carefully when applications open before you start any work you're hoping to get reimbursed for.)

Confirm your fire hazard zone. CAL FIRE publishes Fire Hazard Severity Zone maps. The grant program is for homeowners in ZIP codes that overlap with high or very-high zones. You can look up your own address on the CAL FIRE FHSZ Viewer. Note that the ZIP code overlap rule means even if your specific street isn't in a high-severity zone, you may still qualify if any part of your ZIP code is.

Get bids from licensed contractors now. Roofers, fence contractors, and arborists are going to see a lot more demand once the grant portal opens and homeowners realize what's available. Get bids in hand before the rush.

Track your insurance discount eligibility separately. The grant pays for the work; the insurance discount comes from your carrier under the Safer from Wildfires regulations. They're related but separate. After you complete qualifying work, you'll need to request the discount from your insurer with documentation — it's not always applied automatically.

Why this is worth doing even if you don't get a grant

Two reasons, beyond the obvious one of fire safety.

The first is that insurance access is now genuinely tied to mitigation status in California. Some recently introduced bills would go even further — including one that would require insurers to write or renew policies for homeowners who've completed specified hardening measures, with insurers facing potential suspension from new business in California for up to five years if they refuse. Whether that bill passes or not, the trajectory is clear: documented hardening work is becoming a kind of insurance currency.

The second is that home hardening adds value at resale in a way it didn't five years ago. Buyers in 2026 are asking questions they weren't asking before — has the roof been replaced, what kind of vents does it have, what's in Zone 0, what's the insurance situation. Sellers who can answer those questions clearly, with documentation, are closing deals faster than sellers who can't.

The work itself isn't dramatic. It's not a major renovation. Most of it is the kind of practical, mostly-weekend project that homeowners across LA used to consider boring and skip. In 2026, it might be the single highest-return improvement you can make to your home.

The grant program is meant to help. The application opens in spring. Worth being ready.

This post is for general information only. Eligibility, grant amounts, and program rules for the California Safe Homes grant program are still being finalized by the California Department of Insurance. Check the CDI website for the most current information before starting any work you're hoping to fund through the program.