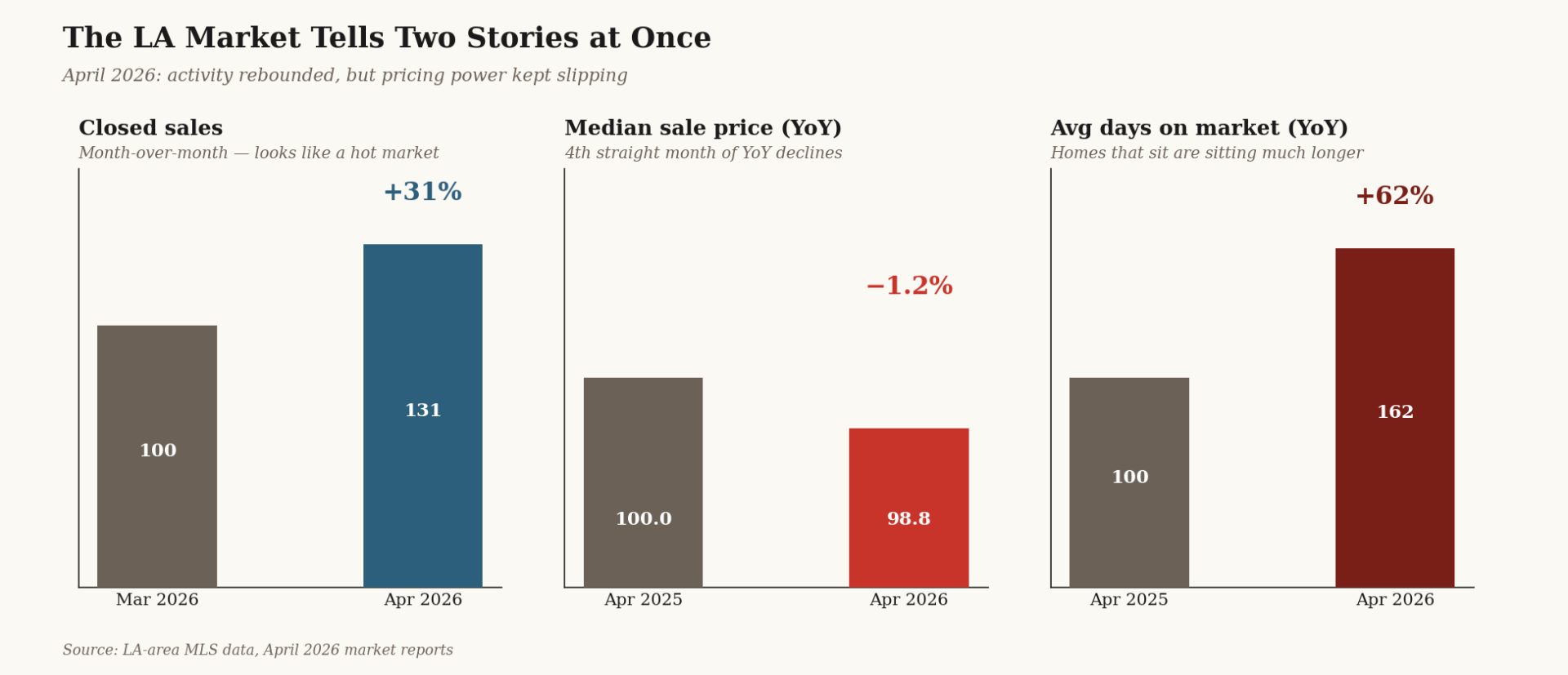

The two markets within the market

If you actually look at LA listings closing in spring 2026, they fall into two distinct categories.

The first category is homes that go pending in under three weeks, often with multiple offers, sometimes selling at or above asking. These properties are well-prepared, accurately priced from day one, presented with professional photography, and have done the unglamorous pre-listing work that buyers are now scrutinizing — inspections, repairs, insurance documentation, disclosures.

The second category is homes that sit. They get showings, they get traffic, but offers don't come. Eventually the price gets cut, then cut again. By the time a buyer makes an offer, it's well below the original list price, and the seller has lost negotiating leverage entirely. Days on market stretches well past 60.

There's almost no middle ground anymore. The pattern that defined much of the LA market in the late 2010s and early 2020s — where most homes sold within 5–10% of asking after a few weeks — has split apart. Now homes either move quickly and well, or they sit.

What's driving this

Three things, mostly working together.

The first is buyer payment sensitivity. With 30-year mortgage rates around 6.30% in mid-April 2026 and home insurance costs in California climbing fast, monthly payments are tight in a way they weren't five years ago. Buyers are doing math — and that math is unforgiving. A 5% pricing mistake by the seller doesn't translate to a slightly slower sale; it translates to the buyer's payment crossing their actual affordability threshold and the property dropping out of their search entirely.

The second is information. Today's LA buyers are sophisticated in a way that genuinely matters. They're looking at price-per-square-foot comparisons, days on market for similar listings, recently closed sales versus list prices, and adjacent micro-markets. They know what fair value looks like. Aspirational pricing — "let's start high and see what happens" — used to work because some buyers would meet sellers there. Now buyers just don't engage. The listing sits.

The third is the new variable that wasn't a factor a few years ago: insurance and risk. Buyers are asking questions about roof age, home hardening, fire zone status, and prior claims that simply weren't part of the conversation pre-2025. A property without good answers to those questions takes longer to sell, even at a reasonable price. A property with great answers can outperform comparable listings nearby.

What homes that actually sell have in common

Looking at the listings that are moving fast in this market, a clear pattern emerges. Five things tend to be present.

The list price aligns with recent closed sales, not active listings. This is the most important one. Sellers and their agents often look at what other comparable homes are currently listed for and price near or above that. The problem is that those listings might also be sitting. The right reference point is what comparable homes have actually sold for in the last 60 to 90 days. In a softening market, recent closed sales are usually below recent list prices, and that gap is where most overpriced listings get stuck.

Professional photography and presentation. This sounds obvious, but the gap between average and excellent listing photos in 2026 is enormous, and buyers respond to it. Drone exterior shots, twilight photos, professional staging or at minimum thoughtful furniture placement, and a property video — these aren't extras anymore. They're table stakes for a competitive listing. Most LA buyers' first interaction with a home is on their phone screen, and the listing either earns the click-through to the full listing or it doesn't.

A pre-listing inspection. Sellers used to wait for the buyer's inspector to find problems, then negotiate. In a slower market, that strategy backfires — buyers use inspection findings as leverage to renegotiate or walk. Sellers who get their own inspection done before listing, fix the obvious issues, and disclose the rest upfront tend to face less renegotiation and fewer collapsed deals. The cost is typically $400–$600. The deals it saves can be worth tens of thousands.

Insurance preparation. This is the new one, and it's specifically an LA factor. Sellers who can hand a buyer documentation of their current carrier, recent renewals, completed mitigation work (roof age, vent type, defensible space, claims history), and a clean CLUE report give that buyer's broker a much smoother path to securing coverage. That ease translates into stronger offers and fewer escrow problems.

Disclosure done right. California has some of the most thorough seller disclosure requirements in the country, and the difference between a thorough, organized disclosure package and a sloppy one is meaningful. Buyers (and their agents and inspectors) read these. A clear, complete package signals that the seller is serious, has nothing to hide, and is going to be straightforward to deal with. That confidence translates to better offers.

What homes that sit have in common

The mirror image is also clear. Listings that struggle in this market tend to share a few traits.

They were priced based on what the seller "needs to net" or what neighbors got two years ago, rather than what comparable homes are currently selling for. They have lukewarm photography, often shot quickly without staging, and a listing description that reads like it was written in five minutes. They went on the market without a pre-listing inspection, and the buyer's inspection found things that triggered renegotiation. The seller has incomplete answers to insurance questions. And then, after sitting for 30 or 45 days, the price gets cut by some round number — $25K, $50K — that wasn't actually based on a fresh analysis of the market, just a guess about how much to drop.

Each of these things on its own is survivable. Stacked together, they signal to buyers that the property isn't being sold seriously, which makes the buyers who do show interest more aggressive on price.

Pricing in a bifurcated market

The single most common mistake LA sellers are making in 2026 is pricing slightly too high — not wildly high, just enough to put the listing in the wrong bucket.

Here's the dynamic. The first two weeks on market are when a listing gets the most attention from active buyers who are watching their saved searches and emails from their agents. If the price is wrong during those two weeks, those buyers move on, and the listing's audience for the rest of its time on market is significantly smaller and less qualified.

A listing that goes up at $1,250,000 when comparable closed sales support $1,175,000 won't sell for $1,225,000. It'll sit for 45 days, then get cut to $1,199,000, then sit longer, then close at $1,140,000 after a buyer with leverage negotiates hard. The seller would have netted more — and certainly closed faster — by listing at $1,175,000 from day one.

This is the asymmetry that's hard for sellers to internalize: in a bifurcated market, the cost of being slightly overpriced isn't slightly slower sale at slightly higher price. It's much slower sale at lower final price. The math punishes optimistic pricing in a way it didn't in 2021.

What this means for sellers right now

If you're thinking about listing in the next 60 days, three priorities.

Get a pricing analysis based on closed sales in the last 60 days, not active listings, and not what neighbors got in 2022. The market is genuinely different now. Comparables from even 12 months ago are stale.

Invest in the pre-listing work that puts you in the "moves fast" bucket: pre-listing inspection, professional photography, staging where appropriate, complete and organized disclosures, and documentation of any mitigation or improvement work you've done.

Be realistic about the insurance question. Pull your CLUE report, document your roof age and any hardening work, and be ready to provide that information early in the process. Buyers' brokers are increasingly asking for it. Sellers who have it ready close deals; sellers who don't get caught off guard during escrow.

What this means for buyers

The bifurcated market actually creates real opportunity if you're prepared to act.

Stale listings — homes that have been sitting for 45+ days — are where the negotiating leverage lives. Sellers who've already done one or two price cuts are usually willing to negotiate further, and they're tired. The listings that just hit the market and look great are competitive; the ones that have been around tend not to be.

That said, the well-prepared listings move fast for a reason — they're priced right and presented well. If you want one of those, you need to be pre-approved (not just pre-qualified), have your insurance broker lined up to run quotes quickly, and be ready to make a strong offer within 48 hours of seeing the home. Pending sales rose 1.5% in March even as the market cooled overall, which means serious buyers are still closing deals quickly when the right home appears.

The bottom line

The 2026 LA market isn't weak. It's selective. Buyers are still active, still buying, and still paying real money for homes that are priced right and presented well. They're just not paying for everything else.

For sellers, that means treating the listing as a product to be prepared, not a property to be advertised. For buyers, it means being ready to move quickly on the right opportunity and being patient enough to walk away from the wrong one.

The middle ground — the casual listings, the casual offers, the casual approach to the transaction — is where deals are dying right now. Both sides need to bring more to the table than they did a few years ago.

Market data referenced is based on publicly available reports for the Los Angeles area as of April 2026. Local conditions vary significantly by neighborhood and price point — talk to a local agent about the specific dynamics in your micro-market.